Singapore ranks among the easiest places to do business, yet tax rules still catch many companies off guard. Business owners face difficulties with their operations because they must manage three areas, which include filing requirements, deadline obligations and changing regulations. Even small errors can lead to penalties or missed savings.

This guide breaks down taxation services in Singapore clearly and simply. You will learn how tax works through this guide, which explains the required services and shows you how to maintain compliance without stress.

Table of Contents

- How Singapore’s Tax System Works

- Key Business Taxes You Need to Know

- Corporate Tax in Singapore: A Quick Breakdown

- GST Registration — Do You Need It?

- What Accounting Services Cover And Why They Matter

- How to Choose the Right Tax Partner

- Common Tax Mistakes Businesses Make

- Conclusion

- FAQs

How Singapore’s Tax System Works

Singapore operates a tax system that requires businesses to pay taxes only on their Singapore-based income and their foreign income which they bring into Singapore. Offshore income which remains outside Singapore territory will not be subject to taxation.

This is one of the reasons Singapore remains one of the most business-friendly countries in the world. The flat corporate tax rate of 17% is already competitive.

All tax matters in Singapore fall under the jurisdiction of the Inland Revenue Authority of Singapore (IRAS).

Key Business Taxes You Need to Know

| Tax Type | Rate / Threshold | Who It Applies To |

| Corporate Income Tax | 17% (flat) | All companies with chargeable income |

| Goods & Services Tax (GST) | 9% | Businesses with >S$1M annual turnover |

| Withholding Tax | 10–15% (varies) | Payments to non-residents |

| Stamp Duty | Varies | Property and share transfers |

| Personal Income Tax | 0–24% (progressive) | Sole proprietors, directors, employees |

Corporate Tax in Singapore: A Quick Breakdown

The business tax services system of Singapore currently stands as one of the most appealing tax systems which exists throughout the world.

The 17% Rate Isn’t Always What You Pay

Most companies pay lower taxes than the 17% headline rate because they receive tax exemptions. The tax rate reductions from these programs provide greater benefits during the initial years of operation.

Tax Exemptions for New Companies

New companies receive substantial tax benefits during their first three operational years. The first S$100,000 receives 75% tax exemption, and the next S$100,000 receives 50% tax exemption.

Tax Exemptions for Established Companies

Established companies obtain partial tax relief through tax exemptions. The first S$10,000 is 75% exempt, and the next S$190,000 is 50% exempt.

Filing Deadlines You Cannot Miss

You must file Estimated Chargeable Income (ECI) within three months after your financial year-end. The submission of Form C or Form C-S must occur before the deadline of 30 November.

Penalties for Late Filing

The imposition of fines and penalties occurs when people miss scheduled deadlines. The penalties will become more severe if your business continues to delay its operations.

GST Registration — Do You Need It?

GST can impact your pricing, cash flow, and compliance. So, it is important to know when and how to register.

The S$1 Million Threshold

You must register for GST once your taxable turnover crosses S$1 million in a 12-month period or is expected to do so soon. After registration, you charge 9% GST and file returns every quarter.

- Applies to both past and projected revenue

- Includes most goods and services supplied

Voluntary GST Registration

Even if you are below the threshold, you can choose to register. This often helps businesses that deal with GST-registered suppliers.

- Allows you to claim input tax on purchases

- Improves business credibility with partners

What Happens If You Don’t Register

Failing to register on time can lead to a serious financial impact. Authorities may step in and enforce penalties.

- IRAS may backdate your GST registration

- You must pay the uncollected GST yourself

What Accounting Services Cover And Why They Matter

Many business owners think accounting is just bookkeeping. In reality, good accounting services cover a much wider range of work.

What Accounting Services Cover

- Bookkeeping and financial record maintenance

- Preparation of financial statements

- Payroll processing and CPF contributions

- GST filing and compliance

- Corporate tax filing (ECI and Form C/C-S)

- Annual return filing with ACRA

- Advisory on tax planning and structuring

Why These Services Matter for Your Business

Running a business in Singapore means dealing with constant deadlines. ACRA filings, IRAS submissions, GST returns, and CPF payments all follow strict timelines.

Because of this, many companies choose to outsource accounting. It helps avoid penalties, reduces stress, and ensures everything stays on track.

Related Post: Corporate Secretarial Services: Why Every Business Needs Them in 2026

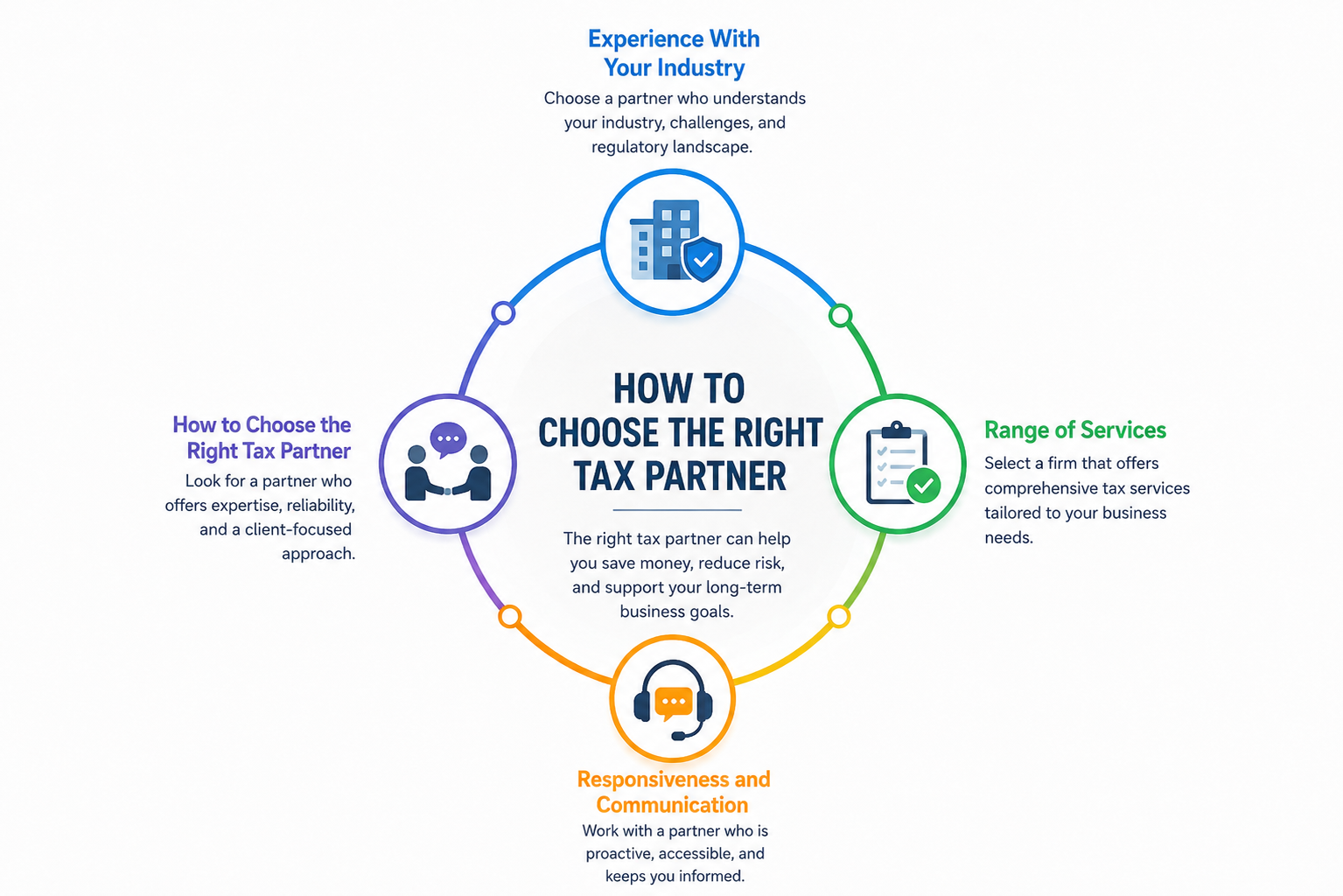

How to Choose the Right Tax Partner

The process of selecting an appropriate tax partner for business tax services will determine the operational efficiency of your business activities.

Experience With Your Industry

Tax regulations differ among various industries, which makes it essential to have industry-specific knowledge. A firm which understands your industry provides better guidance to you while helping you avoid expensive errors.

Range of Services

The firm should provide advanced services because your organisation will require additional support as it develops. This system allows you to handle all tasks through a single platform, which provides uninterrupted service.

Responsiveness and Communication

You need clear answers when tax issues arise. The trustworthy partner delivers fast responses while using straightforward language to explain concepts.

Common Tax Mistakes Businesses Make

Even well-run businesses slip up on tax matters. These mistakes can lead to penalties or missed savings if not fixed early.

- Claiming non-deductible expenses: Private costs, fines, and some entertainment claims can trigger penalties if reported wrongly.

- Mixing capital and revenue expenses: Confusing equipment costs with regular expenses affects both tax and accounts.

- Missing valid deductions: Many businesses overlook claims like startup costs or approved tax schemes.

- Late or incorrect GST filing: Errors in returns, wrong claims, or delays often lead to IRAS penalties.

Conclusion

Singapore maintains a competitive tax system which operates through its effective design. The process of navigating corporate tax exemptions, together with GST compliance and annual filings, requires dedicated effort along with suitable assistance.

Business owners who want to achieve tax compliance while reducing their tax expenses and maintaining their business operations should consult experts. Tan, Chan & Partners offers a full suite of taxation services in Singapore, from bookkeeping to corporate tax advisory.

Reach out today for a conversation about how they can support your business — no obligation, just clear answers.

Frequently Asked Questions

What is the registration deadline for GST in Singapore?

Businesses must register for GST when their taxable annual revenue reaches S$1 million, or they anticipate crossing that limit within the upcoming year. Businesses that fall below this revenue threshold can choose to register voluntarily.

What are the consequences of not meeting a tax filing deadline in Singapore?

IRAS handles late tax submissions with strict enforcement procedures. Your ECI or Corporate Income Tax Return deadline violation will result in a base penalty. The authorities will impose estimated tax assessments and additional fines for continuous non-compliance.

Does Singapore’s territorial tax system provide advantages to foreign investors?

Yes, in most cases. The territorial system enables Singapore to exempt most foreign income from taxation unless it has been brought into the country with specific requirements.

Does a Singapore company have the right to deduct all its business expenses from taxable income?

No. The tax code allows deductions for expenses that businesses spend entirely to generate income. The tax code prohibits the deduction of private expenses, most capital expenditures, and certain entertainment expenses.